This guide helps banking leaders bridge the gap between customer expectations and the current market services that are relevant today. It's a roadmap for survival, because as a bank, you must digitally transform now or risk becoming obsolete.

When was the last time you visited your bank? You probably don’t remember, or you don't have the best bank account. According to Coinlaw as of 2025, “66% of the global population has access to mobile banking, with the fastest growth seen in India, Nigeria, and Bangladesh”. All thanks to their smartphone affordability and fintech innovation.

Things could have been much better, and that is why by the end of 2025, you’ll see more than 89% of banks have their own mobile app, and those who don’t will become obsolete; we have no doubt about that. Now the very simple question arises: If you’re a bank, in what direction should you look? Is an app enough to sustain today’s customer needs?

The answer is a big “NO”; you can’t just rely on a basic mobile banking app today. For years, the banking industry has played by its own rules. However, those rules no longer apply; today’s user is not comparing your banking app with just other banking apps. They want the intuitive design of Uber, not just that, but also the personalization of Netflix, and the convenience of Amazon. They are looking for smart AI features to enhance their own experience. But how do you achieve all that? The answer is Digital Transformation, and you’re in luck because this article will give you a complete roadmap of digital transformation in banking.

60-Second Summary

The Problem: The standard of banking has changed. Customers now demand an innovative and secure solution.

They want an "anytime, anywhere" experience, and they're willing to switch banks if their needs aren't met.

The Fix: Banks must opt for an "Omni-Channel" experience where the customer's journey is perfectly connected across all touchpoints.

The Plan: There are four steps of operation to achieve digital transformation in banking.

Have a customer-centric vision.

Build an integrated technology base.

Applications of smart AI in high-value tasks.

Driving cross-functional teams to transform the company culture.

The purpose: In the future, a bank will be proactive, hyper-personalized, and have an AI-First approach, anticipating the needs of its clients.

Why Do Banks Need to Digitally Transform Themselves?

“I am aware that my data and loyalty are valuable. Reward it with improved rates and personalized offers rather than a generic points program."

Give me anytime, anyplace access

90%

“Banking is not a destination but a utility. Banking hours no longer count. This year, I anticipate 24-hour control of any device. As a User, I don’t want you to overcomplicate security measures; find a resolution that gives me peace."

Understand Me as Your Customer

33%

“I am not a number. Use my history to customize my experience and eliminate the need to repeat myself."

Give me advice on wealth-building

66%

“Don't just hold my money; help me grow it. Be my financial coach, not just a vault."

What Would Be a Good First Step for Banks?

Currently, many banks are operating on a “multi-channel model”, which means many banks have a website, mobile app, and their branch. All of them are working in different silos, which is inefficient, not cost-effective, and not the outcome you’re looking for. To understand what it means to work with a multi-channel model, look at this example

“

A customer might start a loan application online, only to be told they have to start all over again when they visit a branch for help. This creates a disjointed and broken experience.

”

You should opt for an Omnichannel approach, where everything is tightly integrated. I’d give you the financial logic and try to make it simple for you to get what I’m saying:

It cuts expenses: When you make a cellphone transaction. It usually incurs the bank an average cost of only 10 cents. An ATM transaction costs 1.25. Now imagine each of your interactions administered under a low-cost digital channel is a direct cost saving.

It promotes new ways of doing things: A study by Publicis Sapient indicates that 46 percent of individuals conducting their financial transactions online switch across devices before they finish a task. This reality can only be catered via a seamless, omni-channel journey.

“

When customers cannot complete the transaction in the channel of their choice, they hop from one to another channel and unfortunately, the next best channel is usually the more expensive channel: commonly call center.

”

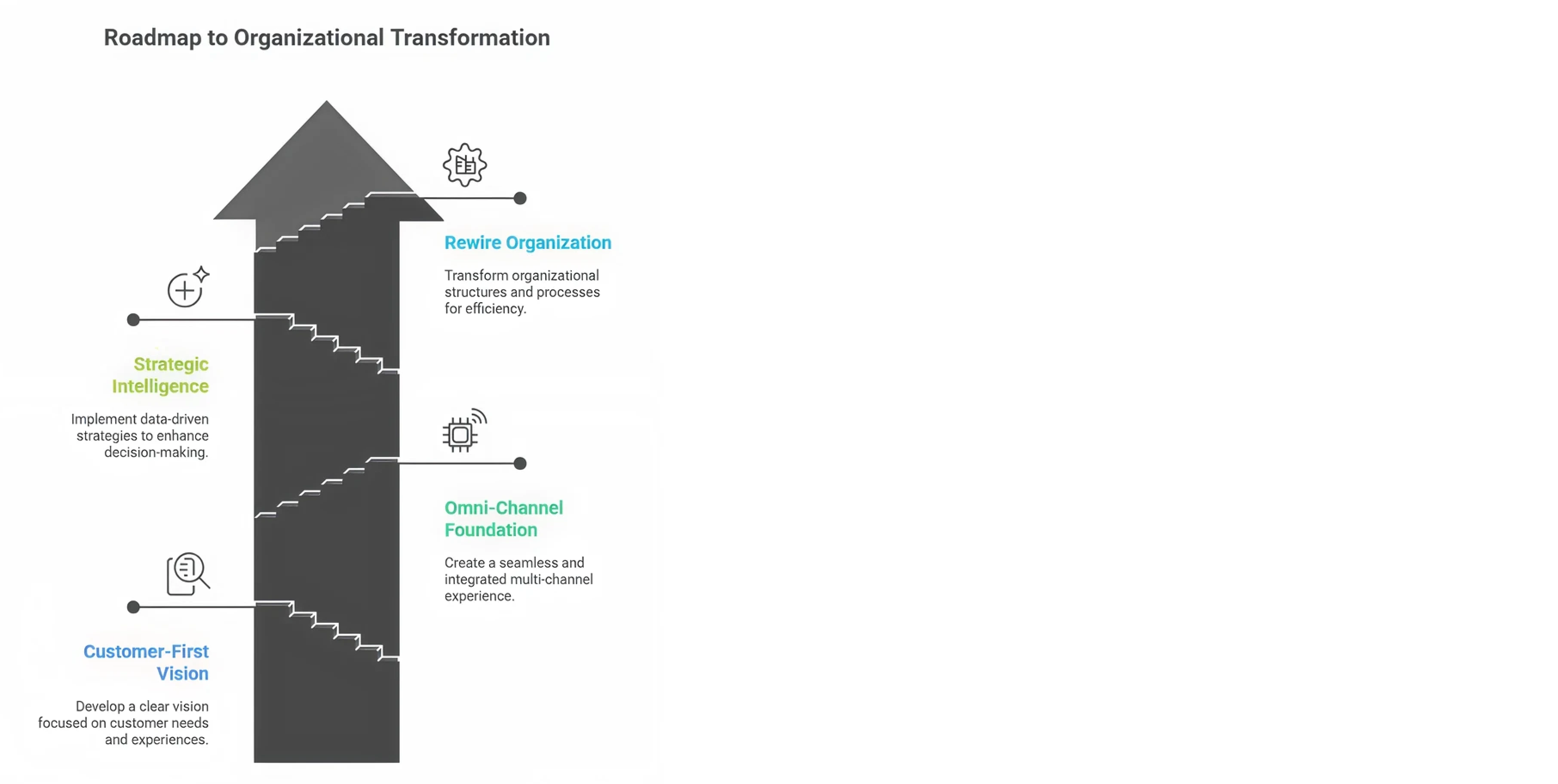

The Action: Your Four-Step Roadmap to Digital Transformation in Banking

Understanding the "what" and "why" is easy. The "how" is what separates the winners from the rest. Here is a clear, actionable roadmap to rewire your financial institution for today.

Step 1: Establish a Customer-First Vision

At BigOhTech, we have led multiple transformations, one of the biggest learnings we had over time is that transformation fails when it’s treated as an IT project. It must be seen differently, like a business-led initiative where you see high-level commitment from the C-suite.

Set a Bold, Bank-Wide Vision: We know changes take time, and to implement those, people now require teams with the modern skill set. You can’t aim for anything small; you have to reimagine how the entire domain would look. You’d have to assess their risks, sales, operations, and how they’d fit in today.

No More Silos: everybody knows that a siloed organization can’t act quickly or take advantage of opportunities. When information isn’t freely shared, your business can’t make informed, data-driven decisions. Inventory, supply chain, distribution, marketing, and sales suffer when teams don’t collaborate, and the idea is to gel all of them together and come up with concrete resolutions to avoid bottlenecks. This is very much possible if banks start seeing the customer not as the channel, but as the center of every decision.

Step 2: Build the Omni-Channel Foundation

You cannot build a skyscraper on a weak foundation, can you? Before you can leverage new Gen AI and agentic AI. You must get your data and channels in order.

Integrate Your Channels: Break down the walls between your mobile, online, branch, and call center systems. Create a single, unified view of the customer so the conversation can move seamlessly between touchpoints without losing context. One thing a customer hates is repeating themselves, and trust me, you don’t even need data to verify this information.

Modernize Your Core Tech: Every bank has to use the most efficient cloud platforms to ensure data is accessible "anytime, anywhere". Invest in Big Data analytics to truly understand the "unstated needs" of your customers by analyzing their behavior, not just their transactions.

Step 3: Strategically Layer on Intelligence

With a solid data foundation, you can now deploy AI for maximum impact.

1. Prioritize ruthlessly: Don't dabble with low-value chatbots that don’t even solve half of customer problems; they keep repeating the same thing, and that only hampers the user experience. Focus on new AI agents like “Loan processing AI Agent", “Transaction Monitoring AI Agents”, etc.

2. Deploy a Multi-Layered AI Stack: A successful AI ecosystem has four layers:

an intuitive Engagement Layer (apps and tools)

an intelligent Decision-Making Layer (the multi-agent AI systems)

A Data and Core Tech Layer

Operating Model Layer (the people and processes). Underinvesting in any one of these will "sabotage the entire effort".

3. Enhance Security with Biometrics: Implement technologies like facial recognition and fingerprint scanning. They are more secure and create a frictionless login experience that encourages digital engagement.

Step 4: Rewire Your Organization

Possibly, one of the biggest challenges of digital transformation in banking is that there are so many touchpoints, and organizations struggle to start all of them at once. But you have to start somewhere, right? Follow these two steps to get a better starting point:

Form Cross-Functional Teams: Today, everybody has to be proficient and work towards the same goal. A Bank today needs a highly skilled team of bankers, as well as high-caliber talent in data, AI, and platform technology. When I say skill, they should be able to adapt to today’s market changes and understand that there is a new requirement they must fulfill. This one becomes non-negotiable; everyone has to break down traditional silos and form teams where everyone works towards a unified goal.

Set up a Central AI Control Tower: To prevent a messy and unnecessary duplication of work, have a centralized body that runs things. This has nothing to do with bureaucracy; it is about coordination. The role of this team is to monitor the value, establish enterprise-wide standards, and, most importantly, promote the reusability of the AI assets. For example, a risk model developed in one department must be easily adaptable for another, which can multiply the pace of innovation across all digital transformation in banking and financial services initiatives.

Leaders in banks must make one of the stark choices today. You would be either the creator of the future of your bank or someone who risks getting obsolete in the industry. The technology is complete, the customer demand is at an all-time high, and the roadmap is evident. The reboot is in action, which you need to seriously think about.

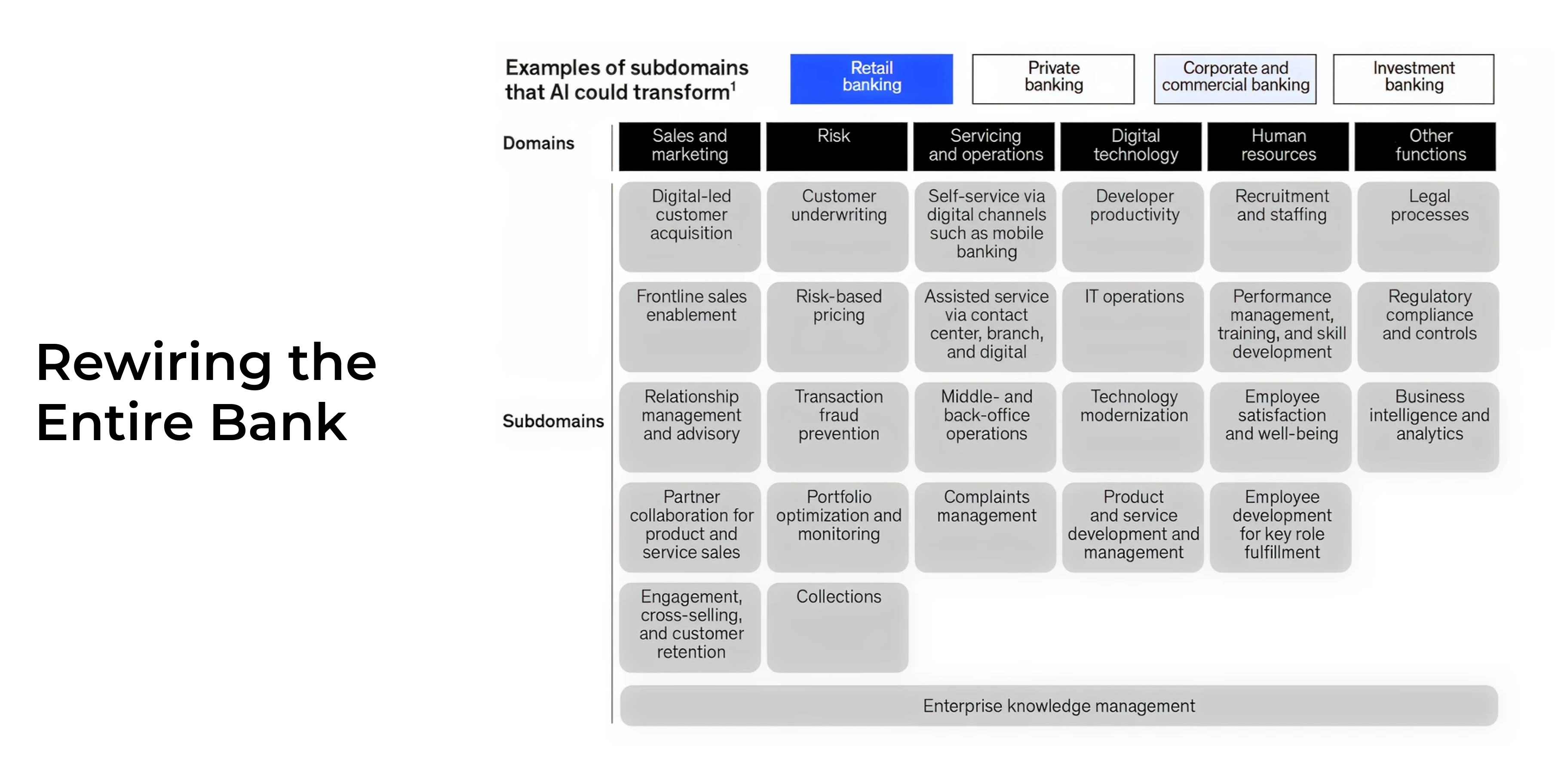

Rewiring the Entire Bank

You must understand that getting real value from AI isn't just about plugging in a new piece of software. It’s way deeper. McKinsey had a great term for it: "rewiring the enterprise." This is a complete, top-to-bottom overhaul of the digital transformation in the banking industry. It touches everything: strategy, operations, tech, even the people you hire. It needs a bold, bank-wide vision to transform entire processes from end to end.

To put this whole evolution into perspective, we can actually map out the journey of digital transformation in banking and financial services across three distinct eras, each with its own philosophy and technology.

Feature

Multi-Channel Banking (The Past)

Omni-Channel Banking (The Present)

AI-First Banking (The Future)

Core Philosophy

Bank-centric; channels in silos.

Customer-centric; integrated channels.

Intelligence-centric; proactive and predictive.

Customer Experience

Inconsistent, requires repeating information.

Seamless, consistent across touchpoints

Hyper-personalized, anticipates needs.

Key Technology

Basic website, separate mobile app.

Integrated CRM, Cloud platforms, Big Data.

Multi-agent AI systems, Gen AI, full-stack integration.

Primary Goal

Provide multiple access points.

Unify the customer's journey.

Automate complex decisions and workflows.

Example

Check the balance online, call a different number for loan info.

Start a loan application on mobile, finish with an advisor in-branch who has all the info.

An AI agent analyzes your finances, proactively suggests a better mortgage rate, and pre-populates the application.

Case Study: Bank of America's Digital Transformation (2025)

In 2025, Bank of America rolled out a huge investment plan of $13 billion in the technology department, of which $4 billion will be invested solely in artificial intelligence.

Hari Gopalkrishnan, Chief Technology and Information Officer, said he expects to push a steady stream of AI-focused releases in the coming months, so as a user, you can expect a lot from this bank. The scheme focused on three main dimensions: improving the effectiveness of the advisors, ensuring customers have an easier time with their phones, and preparing to move towards stablecoin payments.

Let’s get more into detail to understand the new changes or the upcoming ones:

AI Copilots

They already rolled out tools like (ask MERRILL and ask PRIVATE BANK), which allowed advisors to find information, access research, and perform compliance checks within minutes.

Commercial bankers relied on automation as a way to reduce repetitive operations and thus have more time to discuss with their clients.

Upgrading Mobile Banks

Customers began to receive predictive notifications on a forthcoming expense and abnormal account activity.

Increased self-service functionality minimized the support feed, and the product became the primary vehicle of everyday banking.

Stablecoin Readiness

The bank also joined some of the big players in the U.S. to test the use of private stablecoins.

This was impressive, as it provided them with a seat at the table when new payment systems were set up under the scrutiny of regulations.

Early Results

More than 70% of the respondents agreed that AI copilots saved them time.

The complaint levels on mobile banking decreased by 30%.

Automation returned 4 hours of a commercial banker each week on average.

There is significant learning in what today's banks can do; we can see how Bank of America demonstrated that a state-established bank can move to the forefront.

What worked for them?

Continuing to invest in AI and using more powerful mobile apps to manage finances and digital payments. The results are very impressive, and they speak volumes to how crucial it is for a bank to invest in digital transformation today.

How Can BigOhTech Help You Transform Your Bank?

As we look across the business environment, we see too many businesses become stagnant in terms of technology. They have a wonderful vision and idea, but can they actually build it out and get it to work in the digital environment? That’s tough. And that is, really, what we are about to take them through the whole of this process, from the idea to the final product.

We have over 15+ years of experience. We have delivered to some extraordinary clients, such as Jio Money and Nymcard, and put together products that contributed to their successful digital transformation.

So, what is special about what we do? Our dedicated team is our biggest selling point; most of our hires have over 10 years of experience and are very well acquainted with today's tools and technologies. These are the minds that help BigOhTech deliver new emerging technologies, like Artificial Intelligence, Machine Learning, Open Banking & API Ecosystem, Digital Identity & e-KYC Solutions & Data Analytics & Personalization, WhatsApp chatbots, and all the other cool cutting-edge technologies.

We assist in other ways, however. We are ready to outsource our committed developers to other companies who are having a problem, and we do cloud architecture and general IT consultancy to ensure that a business gets the strategy correct. This is all in a bid to enable our clients to provide their customers with the best digital transformation experience.

So yes, when you are approaching the digital transformation and would like to get it initiated quickly and with the correct approach, you must absolutely see us. We’re waiting for you to take your first steps with BigOh!

FAQs on Digital Transformation in Banking

What makes digital change so difficult in the banking industry more than in others?

Banks are highly regulated and face legacy front and back-end systems and have to deal with customer-sensitive information. As opposed to retail or technology firms, they cannot simply replace existing systems in one day. All the steps require compliance, security, and trust, which adds slowness and costs to the process.

How do digital strategies affect the banks due to customer expectations?

Customers expect to receive the modern Amazon experience of personalization and speed in their bank. Banks have to strike this with compliance and data safety. Living up to these expectations and not violating trust is one of the most challenging balancing acts.

Why does cultural / talent shift more of a problem than technology itself?

A bank may purchase the finest technology, but employees are resistant to adopting the change. Moving beyond conventional bank operations to iterative systems, data-combined, and customer-focused is much more difficult than simply signing an IT contract.

What is the cost versus ROI trade-off on banking digital transformation?

Digital initiatives require enormous investments before they pay off (moving to the cloud, automation, AI, customer experience tools). ROI is a long-term project, as it can only be achieved after years of implementation in large banks with complicated infrastructures. You can always consult us to know what the potential return could be, and we would be more than happy to share our transparent pricing, frameworks, and methodologies we use to help you achieve digital transformation.

What are the ways in which regulation and compliance hamper change?

Banks really cannot take risks like startups. All the digital projects, including blockchain-based settlements, AI-based lending, and other activities, have to adhere to the strict financial standards (KYC, AML, GDPR, RBI/Fed/ECB). This is a drag on innovation, but systemic stability is achieved only through this.